The number of deals in consumer packaged goods (CPG) dropped last year to the lowest level in nearly a decade as interest rates remained high and fears of recession loomed, according to Bain & Company’s Global M&A Report 2024. If M&A is critical for market growth, could smaller deals reinvigorate the flow? 👀 According to the report, most innovation in the market is coming from emerging, insurgent brands, not the large leading players; that makes smaller deals necessary. 🤝 We’ve already seen a string of transactions in the small to mid-market space over the past few months including DayDayCook’s acquisition spree, Our Home’s purchase of two brands and production assets from Utz and, most recently, RIND Snacks’ acquisition of Small Batch Organics. Although these smaller transactions may carry a minimized risk compared to a large acquisition – they come with their own unique set of caveats, the Bain team notes. - It can be difficult to determine how to best scale capabilities across both the small brand and the acquirer’s portfolio.

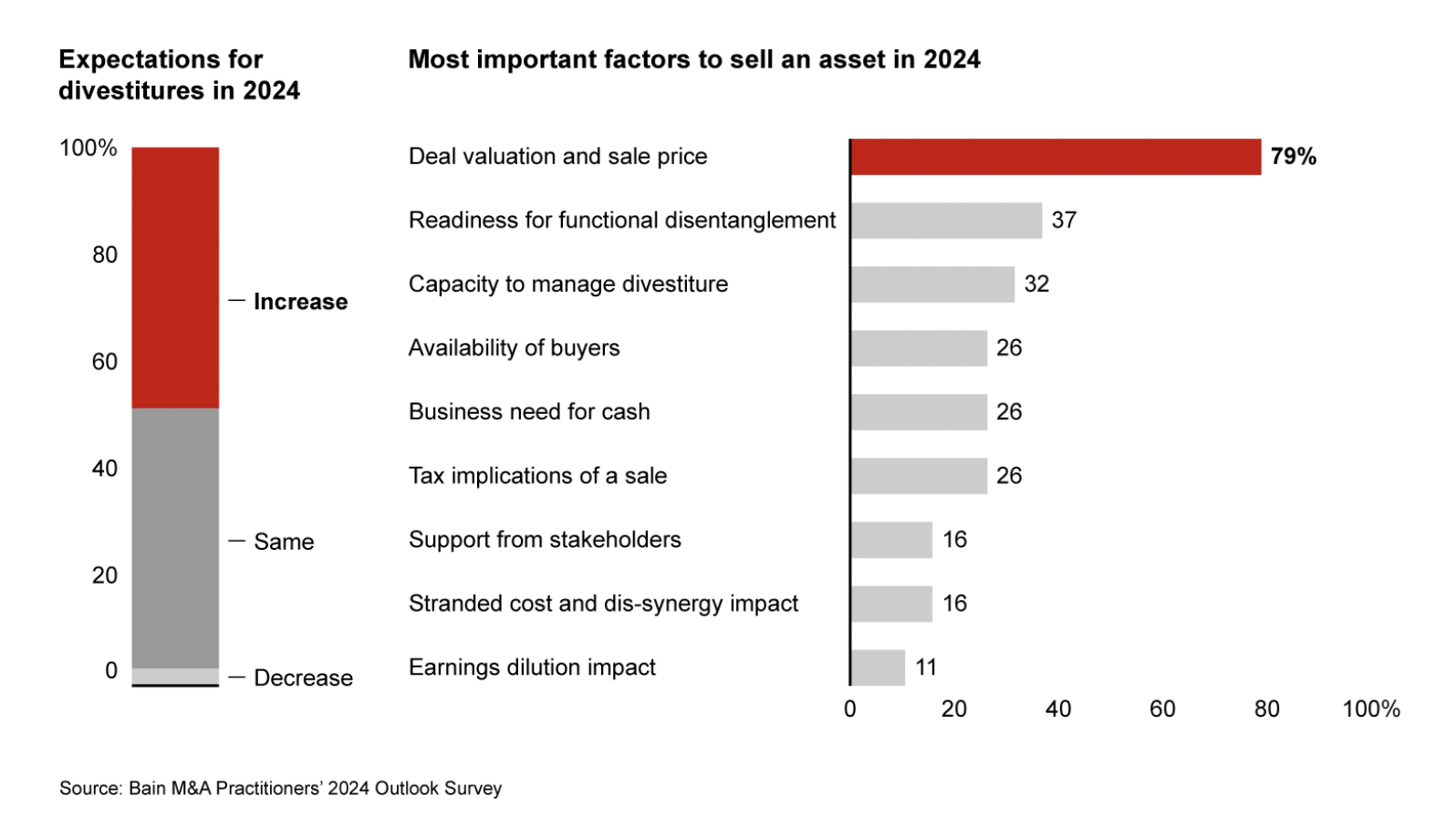

- Underinvested businesses or brands tucked into the portfolio of larger CPGs can be attractive divestiture opportunities, but managing the carve-out can be challenging and time-consuming.

📈 And CPGs will likely need to take more action than buying or selling off parts. The majority of the industry’s recent sales growth has been a result of inflation-driven price increases. As inflation eases, companies will be tasked with returning to profitable, volume-led growth models. 👀 Against that backdrop, Mondelez and Stryve are using SKU rationalization to support margin recovery. But the report highlights that rebounds cannot always be achieved from within. 🤔 They will also require disciplined divestments. Nearly 50% of CPG M&A practitioners told Bain they expect more divestitures in the market in 2024 if the right buyers can be found. Of note for entrepreneurs: The report claims the biggest dealmaking barrier in CPG wasn’t the cost of debt – it was the scarcity of “attractive” assets on the market – followed by a buyer-seller valuation gap and increased competition for assets. 💭 “Integration of smaller assets must be more thoughtful. We have seen many fail because of overintegration, particularly in the early stages. Underintergation, however, can also stifle the generation of synergies. Buyers need to start with a clear articulation of what value needs to be created, leading to which areas need to be integrated (and which don’t),” the report states. ⏩ Looking ahead, the practitioners don’t believe the landscape will change anytime soon. Roughly 35% expect fewer deals next year and 32% expect to see the same number. |